About The Bucket Strategy®

Introduction

As the horizon of retirement draws closer, you need more than just a generic financial plan. You deserve a strategy tailored to your unique aspirations and needs — and that’s exactly where The Bucket Strategy® comes into play, acting as your steadfast compass in your retirement journey.

Investing for retirement income is distinctively challenging compared to simply growing your wealth. Why? Because when you’re aiming for steady retirement income, there’s the risk of market volatility chipping away at your nest egg, especially if you need to make withdrawals during a market downturn. While many firms might advise using the same “pie chart” diversification that works during your wealth-building years, this can pose threats to your savings once you pivot to withdrawing for retirement income.

Enter The Bucket Strategy®, inspired by the robust principles of Liability Driven Investing (LDI) — a professional approach historically reserved for large-scale corporate pension plans and endowments. These plans are obligated to provide a level of annual income to its beneficiaries similar to how retired investors require regular withdrawals from their portfolio to supplement their retirement income needs.

The LDI approach to investing solves the challenge of managing investments over long periods of time while meeting the current income requirements of the investor. It does this by matching the liabilities of the plan to the investments of the plan and thereby matching short-term liabilities with short-term investments and long-term liabilities with long-term investments.

With The Bucket Strategy®, this approach is finely tuned for individuals and families like yours, aiming to provide both comfort and stability in retirement. With its thoughtful design, The Bucket Strategy® shields you from having to sell investments at a loss for immediate income needs, preserving the longevity of your portfolio and ensuring a lasting legacy.

Here's how it works

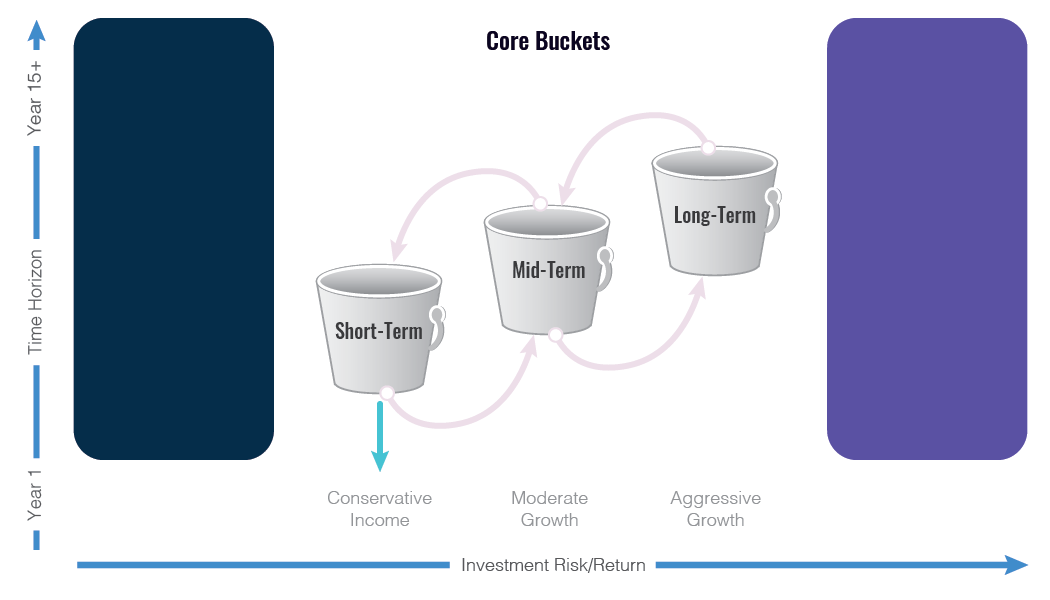

At its core, The Bucket Strategy® segments your retirement portfolio into short-term, mid-term and long-term goals called “buckets”. The purpose is to match your assets to your liabilities by segmenting investments into buckets specifically earmarked to match your current and future retirement income needs.

With The Bucket Strategy®, we embrace a methodology that centers on you. Each bucket is cultivated considering distinct parameters — time horizon, risk tolerance, return objectives and withdrawal requirements — crafting a plan that is personalized and aligned with your individual goals and expectations.

Short-Term Bucket

Investments allocated to the short-term bucket are expected to provide liquidity and near-term withdrawals to supplement your direct income sources such as your social security benefits in order to meet your total retirement income needs.

Mid-Term Bucket

Investments selected to fund the mid-term bucket are designed to replenish the short-term bucket in the future and ultimately provide for future withdrawals.

Long-Term Bucket

Investments earmarked for the long-term bucket are designed for growth, remaining untouched for withdrawals allowing for dividends to reinvest and to take advantage of long-term equity return potential. After the short and mid-term buckets are exhausted, the long-term bucket’s purpose is to refill these buckets and begin the process again.

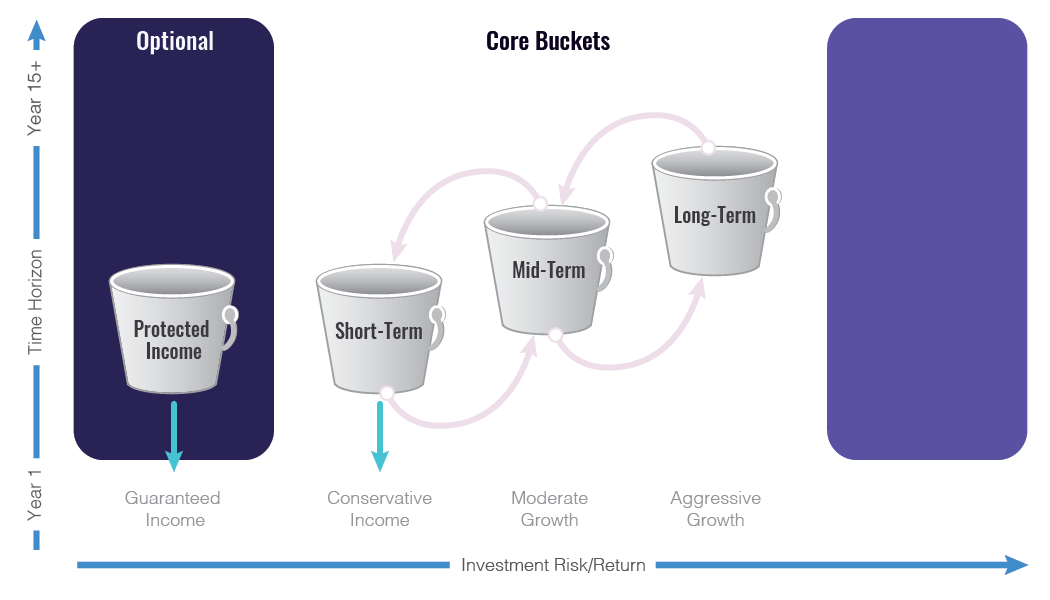

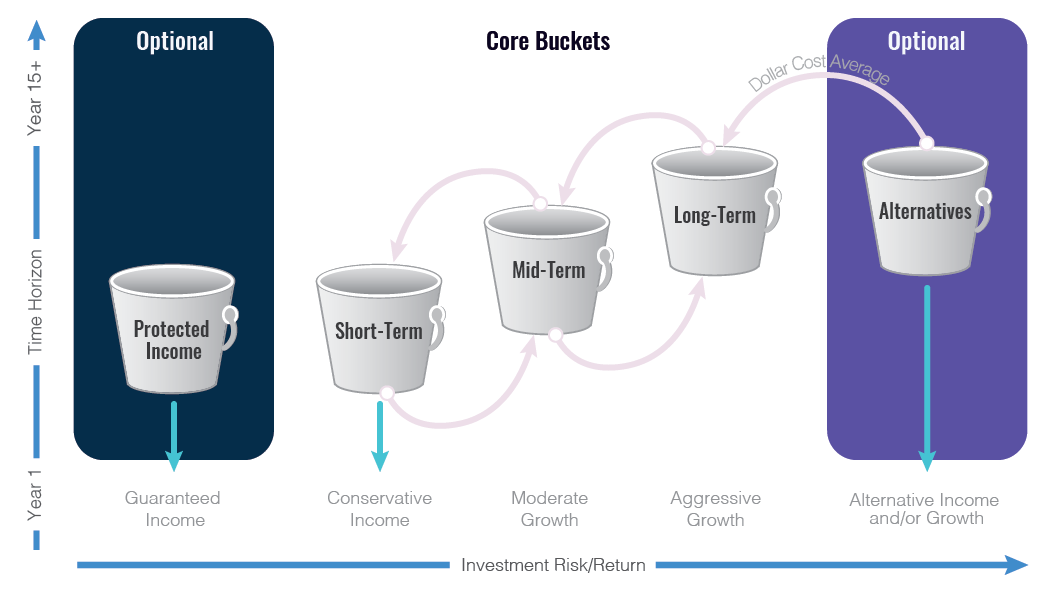

Protected Income Bucket

Allocating a portion of your overall portfolio to a Protected Income Bucket provides a guaranteed source of income that lasts a lifetime. Investors choose to use this bucket to hedge against longevity risk and to fill the gap between their total essential living expenses and their direct income sources such as Social Security and pensions. There are several different types of annuities that offer lifetime income benefits including immediate annuities, fixed indexed annuities and variable annuities.

Alternatives Bucket

Alternative investments add additional diversification to your strategy because they provide investment returns that are different from traditional investments like stocks and bonds. They are intended to ‘zig’ while traditional investments are ‘zagging.’ Alternatives are generally divided into two camps: Alternative Strategies and Alternative Assets. Alternative strategies use sophisticated trading strategies of traditional, public investments to create non-correlated outcomes, while Alternative Assets tend to be private, illiquid assets that require a long-term investment time horizon, such as Real Estate, Private Equity, and Private Credit.

Here’s why The Bucket Strategy® works

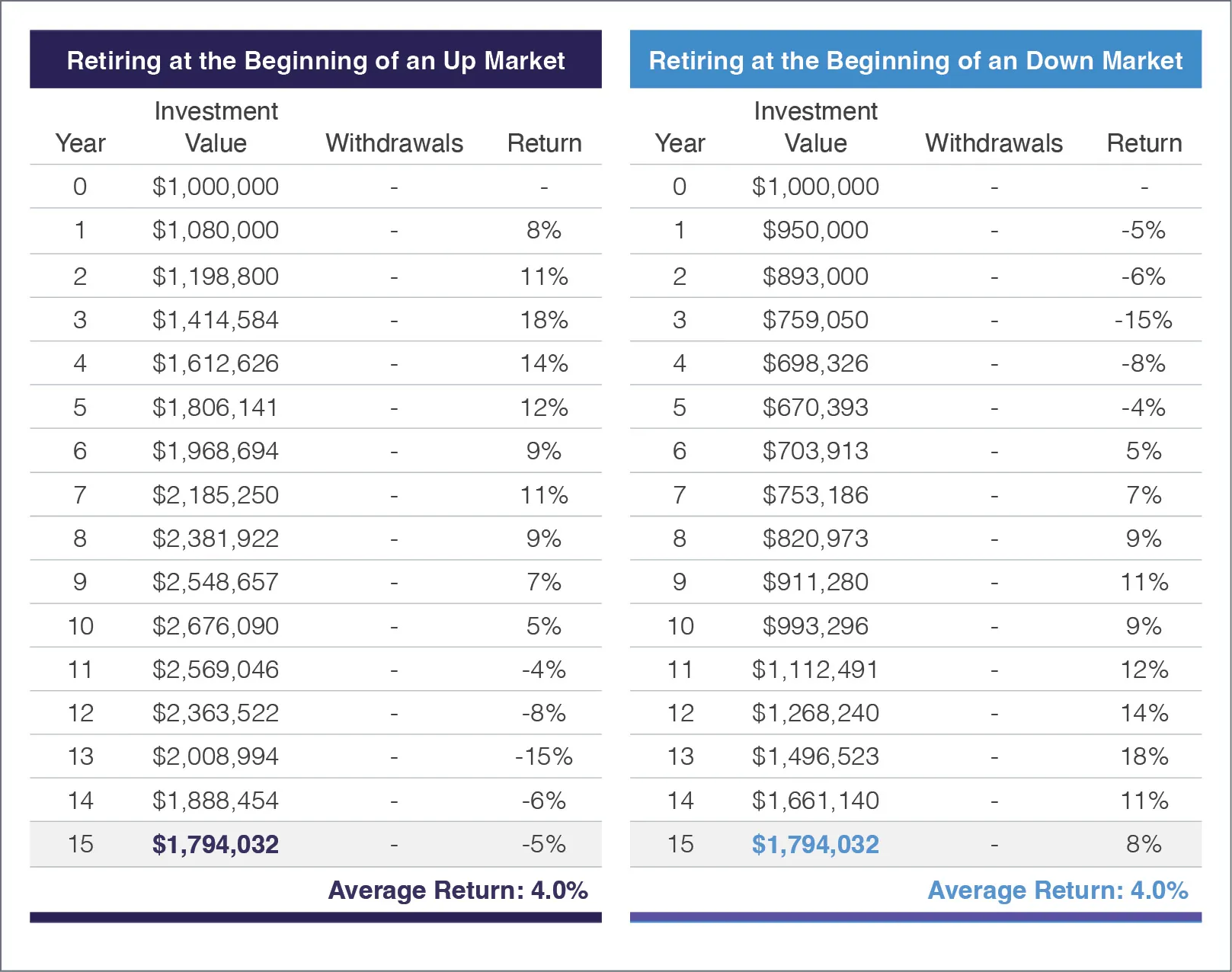

As you edge closer to retirement, the sequence of returns — the order in which your investment returns occur — becomes a critical factor that can significantly influence your retirement nest egg. A downturn in the market just before or early in your retirement can considerably shrink your savings, posing a threat to the financial stability you’ve worked so hard to achieve.

Growing Wealth vs Withdrawing Wealth

Let’s take a look at what happens when you are growing wealth. Does the order in which you get your returns matter?

Example: Growing Your Wealth

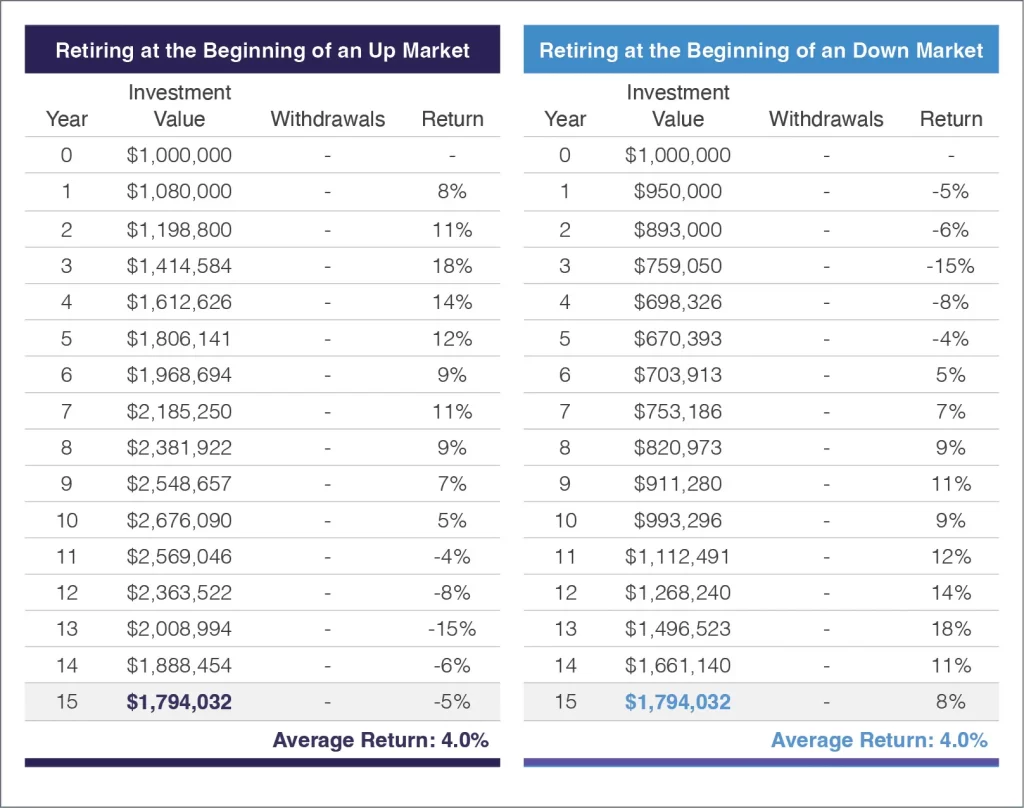

For example, the tables here illustrate two different hypothetical portfolio annual returns over a 15-year period. What’s different is the order of the returns, which has been reversed.

Notice how the average returns are identical even though the order of the returns are not. The ending portfolio values are also the same! It’s surprising that the outcomes are identical even though these two hypothetical investors experienced opposite return sequences.

Example: Withdrawing Your Wealth

Now notice what happens when we decide to take withdrawals from each portfolio. Look how significant their ending investment values differ.

One investor’s ending value is higher than the beginning balance and the other investor may be broke in a handful of years! The order in which you experience returns matters when you begin to take withdrawals from your portfolio.

As your financial advisor, we must assume you will be the unlucky investor retiring at the beginning of a down market, experiencing an unfavorable sequence of returns early in your retirement.

The Bucket Strategy® stands as a vigilant guardian against this risk. Essentially, when drawing your income from the short-term bucket with more stable, conservative investments your portfolio has the potential to avoid the adverse effects of potentially bad return sequences in the earlier years of retirement.

Managing the sequence of returns risk for the first 15 years not only gives you the confidence to remain invested regardless of current market conditions but also allows for flexibility in deciding when or whether to begin a rebalancing protocol. According to research, assuming a 30-year retirement time horizon, “the outcome of a withdrawal scenario is dictated almost entirely by the real returns of the portfolio for the first 15 years” (source: ‘Reducing Risk with a Rising Equity Glide-Path,’ 9/2013, Kitces & Pfau). Therefore, spending from the safer assets first, from your short-term bucket, and tapping into the riskier assets like stocks last, from your mid- and long-term buckets, has proven to be a prudent approach to managing sequence of returns risk.

Leveraging Time and Diversification: The Cornerstones of The Bucket Strategy®

In the ever-fluctuating financial markets, The Bucket Strategy® offers a sanctuary of stability, using the dual pillars of time and diversification to steer clear of market risks and forge a path of sustained growth.

Harnessing the Power of Time

The variability of returns improve with time, meaning that the longer you stay invested, the lesser the risk of encountering a permanent loss. By strategically drawing income from safe and lower volatile investments and placing your growth investments with a longer time horizon, it effectively reduces the risk of capital erosion, caused by needing to sell investments at a loss to fund your retirement income.

Masterful Diversification

Diversification is not just about having a variety of assets; it’s about intelligent allocation that stands resilient against market volatilities. The Bucket Strategy® crafts a portfolio where assets are not only diverse but are orchestrated to work in harmony across the buckets, creating a symphony of investments that can weather market fluctuations with stability and grace.

By unifying time and diversification, The Bucket Strategy® moves beyond mere asset accumulation, ushering in an era of thoughtful financial planning where every investment has a specific purpose.

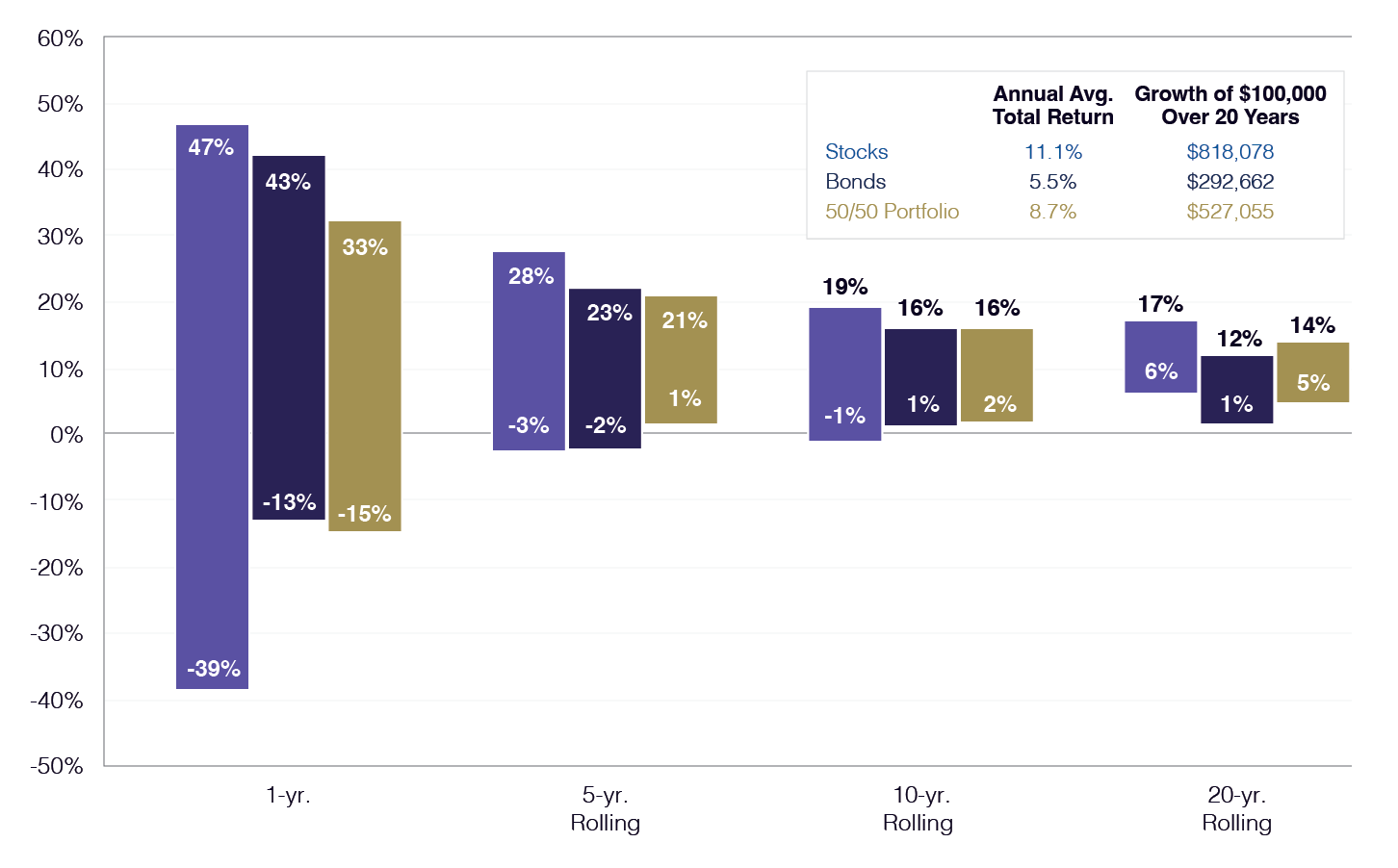

The chart on this page illustrates range of returns for equities, bonds, and a 50/50 split over different time horizons. Note that the longer the time horizon, the risk of loss is reduced and the range of returns narrows.

Source: Bloomberg, FactSet, Federal Reserve, Robert Shiller, Strategas/Ibbotson, J.P. Morgan Asset Management, JP Morgan Guide to the Markets.

Returns shown are based on calendar year returns from 1950 to 2021. Stocks represent the S&P 500 Shiller Composite and Bonds represernt Strategas/Ibbotson for periods from 1950 to 2010 and Bloomberg Aggregate thereafter. Growth of $100,000 is based on annual average total returns from 1950 to 2022.

J.P. Morgan Guide to the Markets – U.S. Data are as of September 30, 2023.

The Protected Income Bucket: A Stepping Stone to a Worry-Free Retirement

Imagine stepping into your retirement with the comforting assurance that all your essential income needs are well taken care of, month after month, year after year. This isn’t just a dream — it’s what The Bucket Strategy® promises through the creation of a personalized Protected Income bucket.

We begin by taking a close look at the regular income you’ll have in retirement — things like social security, pensions, or earnings from rental properties. We compare this with the everyday expenses you anticipate having when you retire. This is where the Protected Income bucket steps in, strategically designed to fill in any gaps, ensuring you have a reliable and steady income to cover all your basic needs.

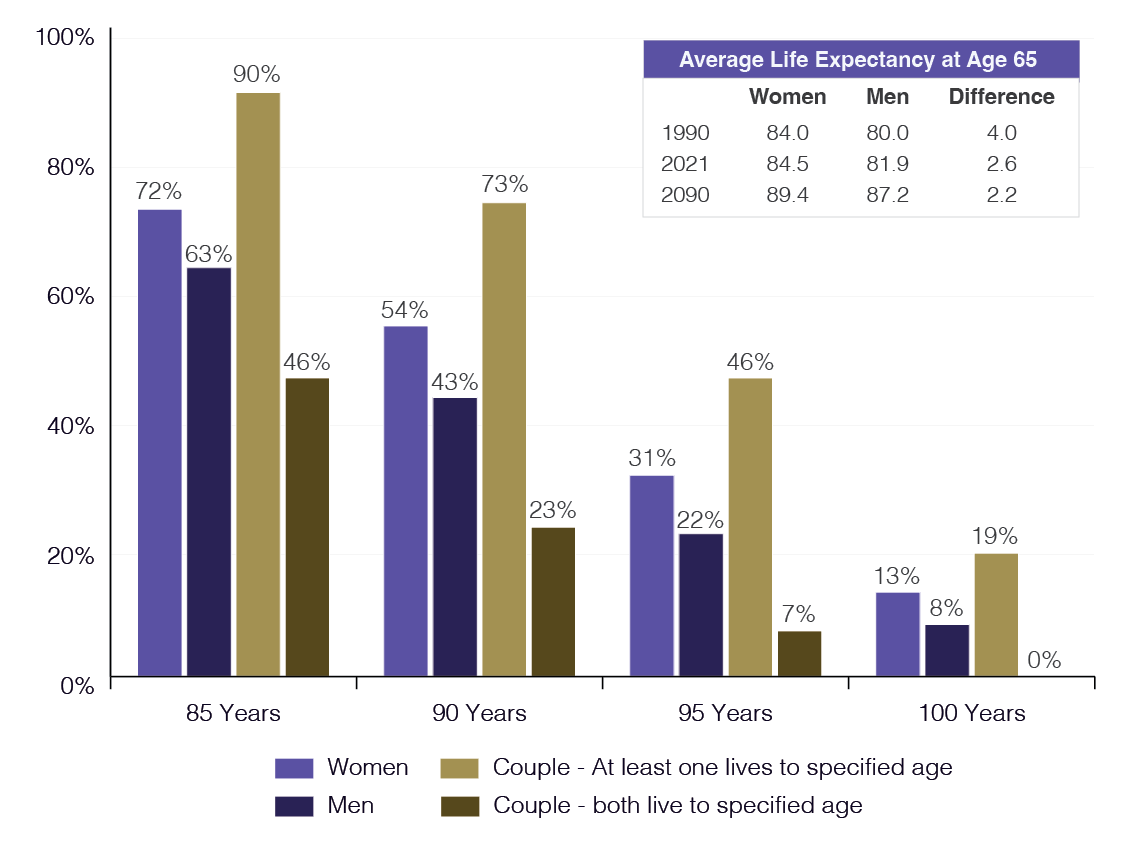

Outliving Your Savings – Longevity Risk

One of the central fears as we age is outliving our savings. With the continued advancement in medicine and life technologies, life expectancies continue to lengthen. A couple age 65 today has a 19% chance that either one will live to age 100.

Source: Social Security Administration, Period Life Table, 2019 (published in the 2022 OASDI Trustees Report); American Academy of Actuaries and Society of Actuaries Longevity Illustrator, http://www.longevityillustrator.org (accessed September 29, 2022), J.P. Morgan Asset Management.

Funding the Protected Income Bucket with Lifetime Income Annuities

Lifetime income annuities act as a buffer against this longevity risk, offering you the peace of mind that comes with guaranteed, lifelong income. It’s an assurance that your essential living expenses are covered, come what may.

Elevate Your Portfolio with Alternative Investments

Harnessing Diversification and Enhanced Return Potential

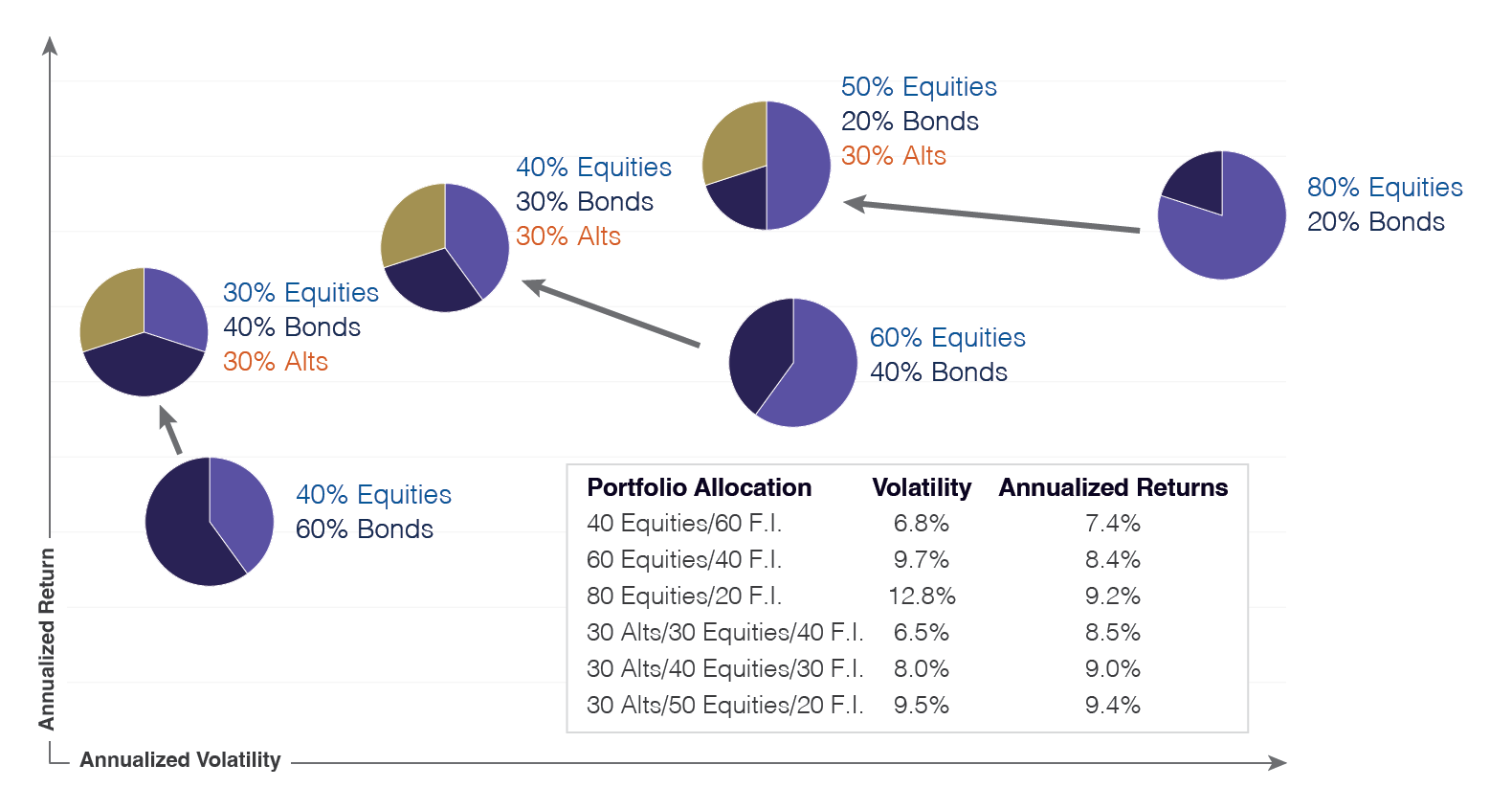

Constructing a resilient retirement portfolio often means exploring beyond the conventional avenues of stocks and bonds. Alternative Investments bring the allure of returns that don’t always move in tandem with mainstream markets: when traditional assets take one direction, Alternatives might very well take another. Moreover, selecting Alternative Investments can deliver appealing income distributions, potentially mitigating withdrawal pressures from your other buckets. This is where The Bucket Strategy® shines by seamlessly integrating Alternatives, providing your financial plan with a multifaceted edge designed to amplify both growth and income.

Source: Bloomberg, FactSet, Burgiss, HRFI, NCREIF, Standard & Poor’s, J.P. Morgan Asset Management. Alts include hedge funds, real estate, and private equity, wiht each receiving an equal weight. Portfolios are rebalanced at the start of the year.

J.P. Morgan Guide to the Markets – U.S. Data are as of September 30, 2023.